ELECTION 2013: Advance voters coming out in droves

It's seemingly counterintuitive for financial institutions to encourage their customers to hold more cash in their accounts. After all, banks and credit unions make money by putting your money to work in financial instruments ranging from mutual funds and stocks to mortgages and lines of credit.

But as economic prospects remain muted in Canada, behind every suggestion from financial institutions for households to put more money aside for a rainy day are growing fears over household solvency.

Canadians are apparently losing their traditional small-c conservative sentiment toward financial risk.

That seems clear from all the talk about record levels of household debt in Canada.

Whether we're buying more expensive homes or borrowing to satisfy our desire to indulge in retail therapy, Canadians seem OK with accumulating debt.

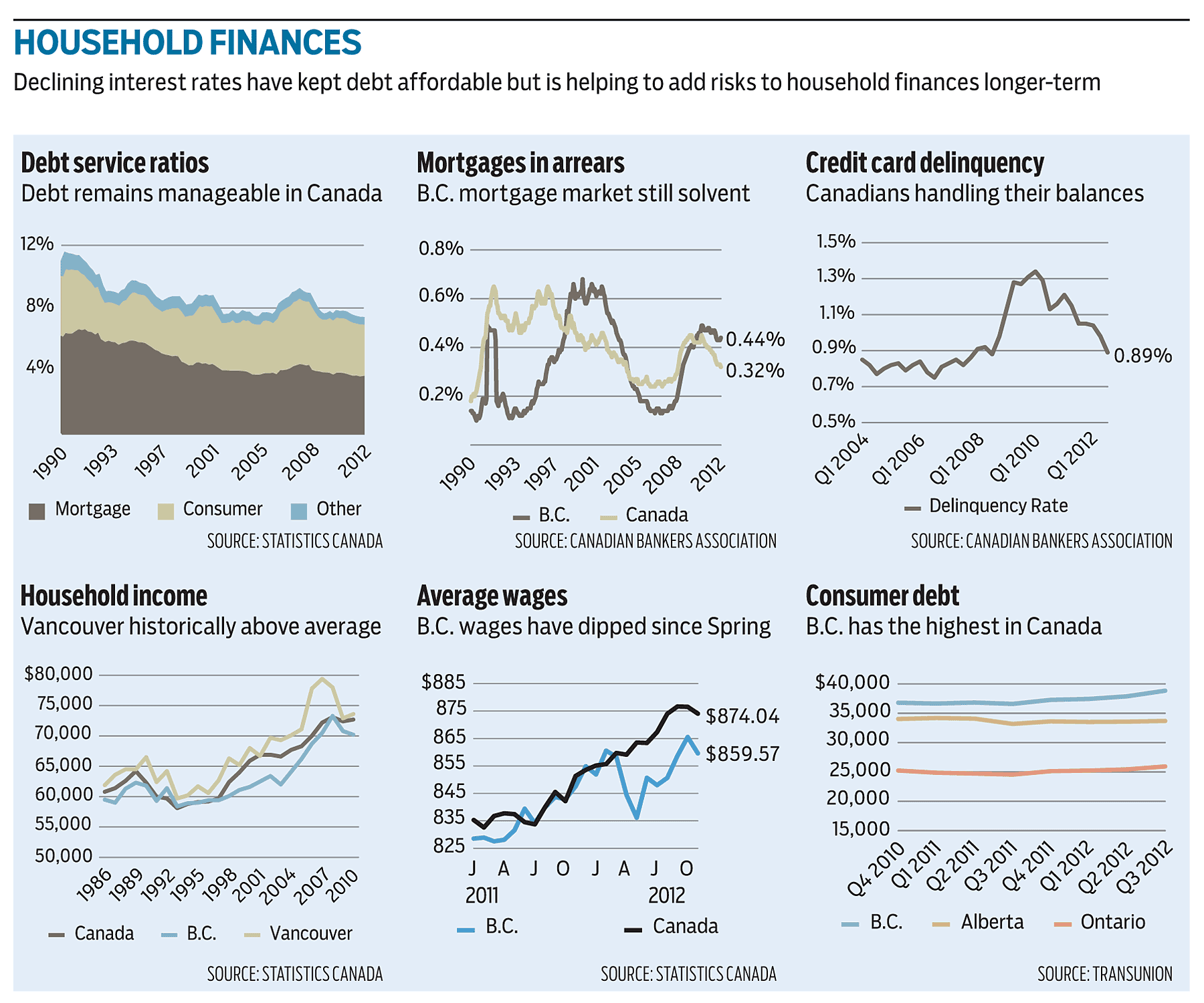

But debt isn't the problem. Not for the vast majority of Canadians and homeowners in B.C. According to Canadian Bankers Association data, less than 0.5% of all mortgages in B.C. are behind on their payments and less than 1% of credit card holders in Canada are delinquent.

And even though overall per-household debt might be rising, the proportion of income needed to service that debt has remained fairly consistent for much of the past decade.

According to Statistics Canada, Canadians have spent on average around 4% of their income to service their mortgage debt and less than that for consumer debt since 2002. An RBC Economics report noted total household debt ratios have remained nearly 1% below the long-term average in Canada for the past five years. And with long-term mortgage rates potentially staying near record lows for several more years, debt is likely to remain manageable for most homeowners across the country. This will be especially true for Canadians who decide to lock in their mortgages for 10 years at a fixed rate of less than 4%, which is currently being offered by various financial institutions and is well below posted five-year fixed rates above 5%.

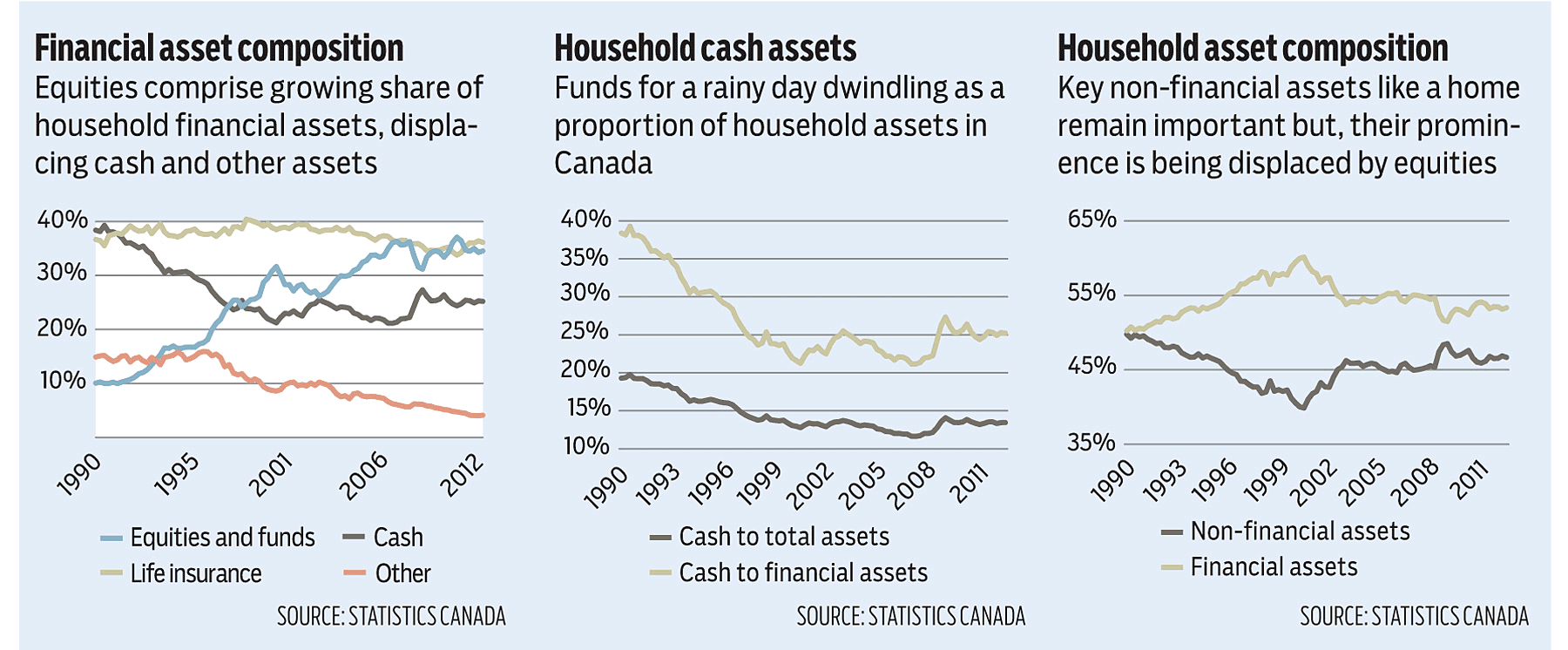

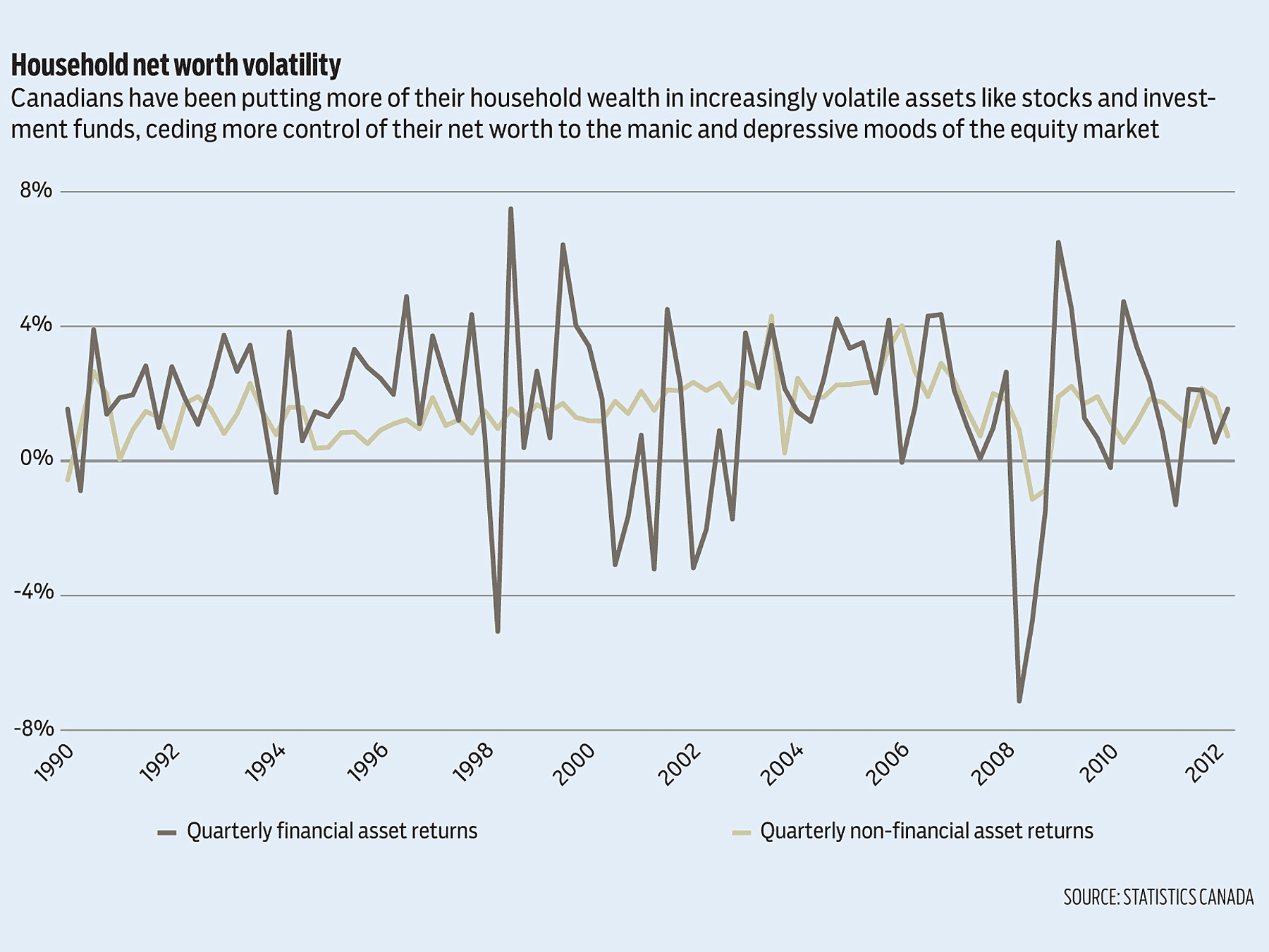

A key risk for households is the source of their net worth, which is increasingly being put in volatile assets.

Vancouverites least prepared with rainy day fiscal fund

Cash has been king in the business world since the financial crisis. Analysts and economists the world over effectively evoke Carl Sagan in noting the billions and billions of dollars in cash sitting in corporate bank accounts instead of being used to expand and stimulate overall employment.

But the levels of cash held by Canadian households have been declining, which poses some worrying risks to the financial health of the country's consumers.

An RBC Economics report noted that Canadians' holdings of cash and deposits have fallen nearly 29% over the past three decades and have dipped below the long-term average since the late '90s. Today, less than 15% of household assets are held in cash. This can be worrisome for a growing number of households that face "adverse economic shocks" like having a key household breadwinner lose his or her job.

This is a significant issue for households in B.C., and particularly in the Lower Mainland, which TD Economics has suggested are the most vulnerable to adverse personal circumstances. Its benchmark report in 2011 noted that B.C. residents had the country's highest debt-service ratio and are the most vulnerable to interest rate increases.

Meanwhile, another TD report noted that 41% of British Columbians don't have any money set aside for unexpected expenses, even though nearly two-thirds said they needed cash to deal with unexpected budget challenges such as being laid off, paying a bill for a sudden medical issue or for urgent home repairs.

For the most part, Canadians have managed to keep their heads above water with their debt because of record low interest rates, and RBC noted that most Canadians could manage a 1% increase in interest rates given the Bank of Canada overnight rate has remained at historical lows for a record period of time because of the sluggish economy.

But the trade-off with low interest rates is that Canadians are putting more of their financial assets in more risky and volatile investments like stocks and insurance products and mutual funds that have a majority of assets in equities. This poses substantial risks in the longer term for Canadian households.

Reliance on stocks threatening Canadian household net worth

As debt grows to record levels in Canada, the financial powers-that-be have paradoxically urged Canadians to take control of their finances. We need to do a better job of controlling our spending. Pay down our debt. Build up our rainy day funds. Save more for our retirement.

But Canadians have been slow to take that advice to heart. Aside from feeling increasingly comfortable with shouldering more debt, they have been accumulating less cash. Canadians are instead betting their financial futures in riskier and more volatile investments like stocks.

An RBC Economics report noted that three-quarters of Canadian household financial assets are now in stocks, insurance products and mutual funds that have a majority of assets in equities - compared with only half in the early 1980s.

Much of this reflects the steady decline of interest rates over the past 30 years. As rates fell, so did returns on traditional fixed-income investments such as government bonds and GICs. To offset these declines, investors have tried to increase investment returns by moving into higher risk assets.

The impact of this move up the risk-return scale was most notable after the 2008 financial crisis. With a greater proportion of retirement nest eggs and household assets in equities, many Canadians have found their net worth fluctuating more wildly than in the past. The report noted that households experienced an average loss of net worth of 10.2% in 2008 following the financial crisis. If investors didn't sell their stocks then, they likely saw their net worth recover in subsequent years - although not everyone (especially those near retirement) stayed in the market to weather the volatility.

With more household wealth in equities, Canadians will likely be forced to prepare themselves emotionally for a long-term rollercoaster. The report noted that because Canadians have been saving less, they have been relying more on capital gains and home price appreciation to bolster their net worth.

With housing prices expected to remain relatively flat over the next few years in B.C. and continued stock market volatility, households with high debt levels and little cash on hand face an uncertain and potentially bleak fiscal future.